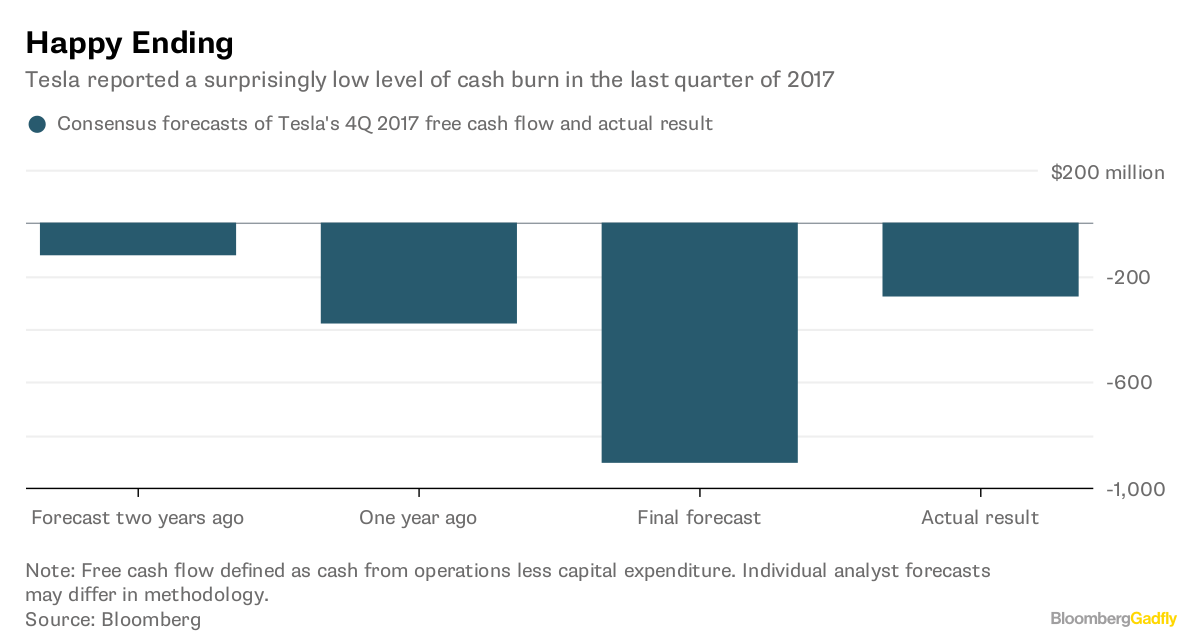

Tesla's free cash flow is usually a tragedy in three acts. Early on, analysts forecast a big improvement a couple of years out. Then, the mood darkens and the cutting begins. In the closing scene, Tesla unveils a reality far worse than was imagined (curiously, the stock-holding audience quite often claps regardless).

But this week's results delivered a plot twist:

Happy Ending

Tesla reported a surprisingly low level of cash burn in the last quarter of 2017

Source: Bloomberg

As I wrote here, though, there were one or two sub-plots beneath. They're worth delving into as we guess at what happens with Tesla in 2018.

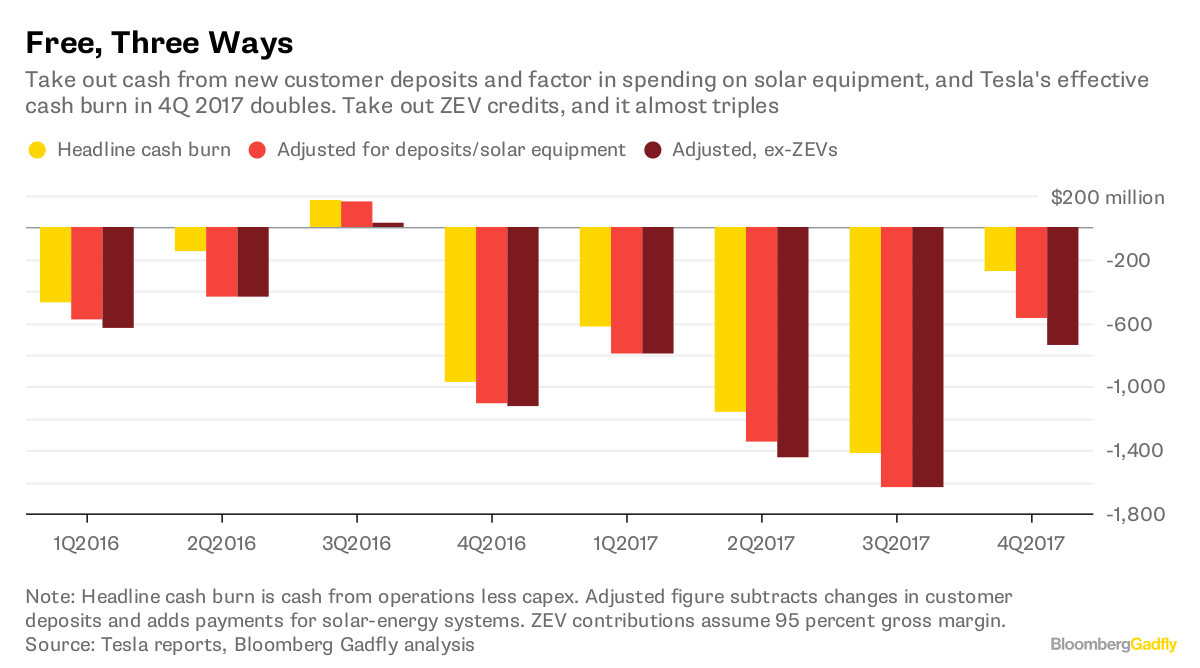

Tesla reports free cash flow as cash from operations less capital expenditure, which is fairly standard. But non-GAAP metrics, while handy, aren't standard; and there are two obvious things to quibble with here (plus one that's less obvious).

First, Tesla includes cash from customer deposits in cash flow from operations. However, they're refundable and increasingly relate to vehicles that may not be delivered for years to come. They're more like cash flow from financing.

Second, Tesla's definition of capital expenditure doesn't include another line item under cash flow from investing: "payments for the cost of solar energy systems, leased and to be leased." This is cash used to buy panels and such to be leased to homeowners and other customers; it has run at about $100-$200 million per quarter since Tesla bought struggling sister company SolarCity Corp. in 2016.

Tesla is right to not include it in capex. But it should still be subtracted from free cash flow as money going to build inventory (Tesla classifies leased solar systems as long-term assets, which is presumably why the equipment doesn't factor into working capital).

There's one more thing: zero-emission-vehicle credits, or ZEVs. Tesla usually has a surplus of these -- it gets them for selling all-electric vehicles -- and can trade them for cash at a very high margin (I estimate 95 percent).

But this revenue is lumpy and unpredictable, and sometimes makes the difference between Tesla missing or beating earnings forecasts -- as in the latest quarter. So it's worth taking them out to look at underlying free cash flow.

Here's how Tesla's free cash flow looks with these adjustments:

Free, Three Ways

Take out cash from new customer deposits and factor in spending on solar equipment, and Tesla's effective cash burn in 4Q 2017 doubles. Take out ZEV credits, and it almost triples

Source: Tesla reports, Bloomberg Gadfly analysis

Adjusted cash burn was more like $600 - $700 million, depending on how you treat the ZEV credits. Factor in the capex that Tesla deferred in the quarter and that would rise to more like $800-$900 million.

None of those numbers are definitively "right" or "wrong." They're just signposts as to why, despite double-digit revenue growth and moderate headline cash burn, Tesla's net debt increased by almost $570 million.

They also underline the role played right now by those customer deposits and Tesla's management of working capital in general. The deposits brought in $168 million; running down inventory and accounts receivables added another $300 million. Altogether, these account for virtually all of the positive $497 million of cash from operations Tesla reported.

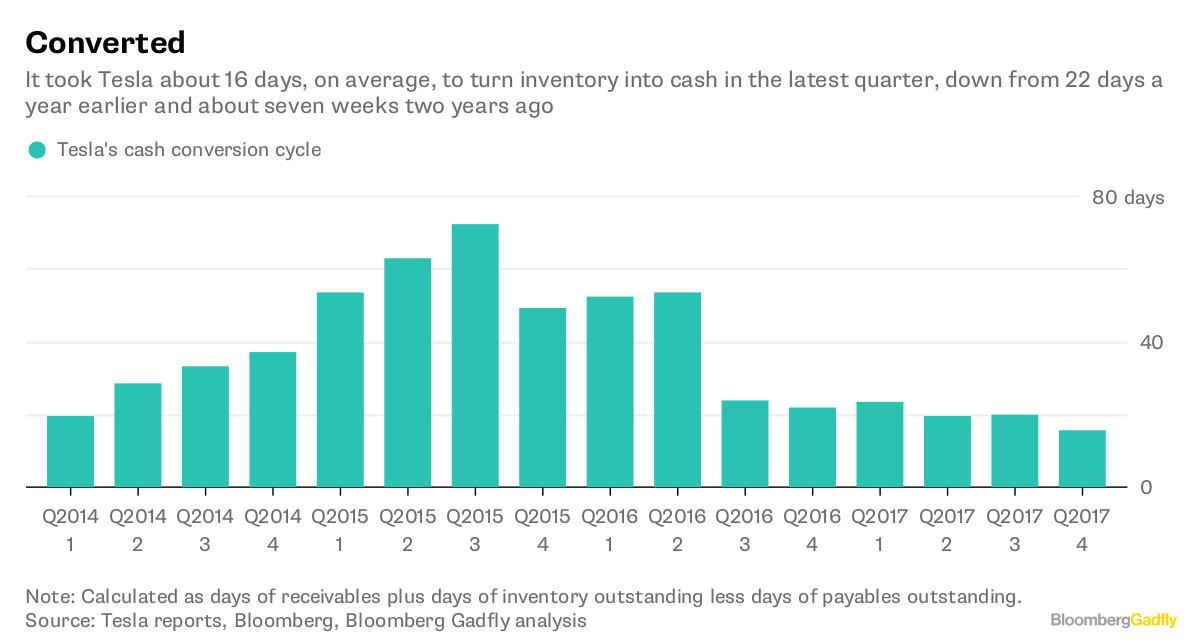

The company's cash-conversion cycle -- how quickly it turns inventory into cash flow -- has accelerated sharply over the past year and a half:

Converted

It took Tesla about 16 days, on average, to turn inventory into cash in the latest quarter, down from 22 days a year earlier and about seven weeks two years ago

Source: Tesla reports, Bloomberg, Bloomberg Gadfly analysis

At the same time, Tesla net working capital -- leaving out cash and short-term debt -- has shifted further into negative territory:

The Low Down

Tesla's net working capital has dipped further and further into negative territory, with a marked shift downward in the fourth quarter

Source: Tesla reports

There's nothing inherently wrong with this; if your business can get free funding from others -- suppliers, depositors -- to run your business, that's great. And all auto-makers try to convert their inventory to cash as quickly as possible, selling cars to captive finance arms, for example, or securitizing leases, as Tesla did earlier this month with a $546 million issuance of asset-backed bonds.

Ultimately, though, issuing more debt and relying on negative working capital ratchets up your funding risk. Tesla's boast of having $3.4 billion of cash was notably close to the top of its results announcement; that amount almost covers the negative net working capital of $3.7 billion (though not short-term debt).

Tesla's CFO acknowledged the limits of working capital windfalls on the earnings call:

We significantly reduced the finished goods inventory of [Model] S and X in Q4, which will not repeat itself going forward. And that was a huge impact on working capital. Customer deposits may not be as well ... However, as the Model 3 ramp continues, the negative working capital needs for that, which essentially create extra cash for us will be repeatable. And we'll continue to keep very tight controls on our accounts receivables and everything else we do to manage cash.

This -- more than credibility, ego, or whatever -- is why Tesla must get that Model 3 production line working properly, and fast. The more Model 3s it can sell and lease-and-securitize (and attract more deposits on), the longer it can keep that working-capital cycle working. As Hitin Anand, an analyst at CreditSights puts it:

This is all contingent on the Model 3 coming through in terms of production.

And with capex accelerating again, raising Model 3 production would not only help Tesla mitigate the burn via working-capital effects, but in another important way: tapping the public markets.

Say Tesla hits its 5,000-a-week target by July. It wouldn't be a silver bullet, but would give bulls a sign of progress. At that point, and with another shiny new product on the horizon -- the promised Model Y crossover -- Tesla might feel emboldened enough to sell more bonds or stock to refill its coffers.

As it happens, on the earnings call CEO Elon Musk noted both his excitement about the Model Y and that gearing up for it would necessitate some spending later this year. For all the drama, it's getting easier to see where this story goes in 2018.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

To contact the editor responsible for this story:

Mark Gongloff at mgongloff1@bloomberg.net

Bagikan Berita Ini

0 Response to "Tesla's Working Capital Must Work Hard To Make 2018 Work"

Post a Comment