GOTHENBURG, SWEDEN - 2019/09/14: An American automotive and energy company that specialises in ... [+]

Tesla (NASDAQ: TSLA) posted a stronger than expected set of Q1 2020 results, despite the coronavirus pandemic, with revenues growing by ~32% year-over-year and adjusted profits coming in at $227 million, versus a loss of about $494 million a year ago. While the company benefited from strong deliveries of the Model 3 and a production ramp at its Shanghai factory, much of the improved profitability came from higher sales of emission credits which soared to about $354 million from an average of about $150 million over the last four quarters. If not for the spike in regulatory credit sales, Tesla would likely have barely broken even. Below, we take a look at how sales of regulatory credits have helped Tesla and why we believe the near-term outlook for the company looks quite challenging.

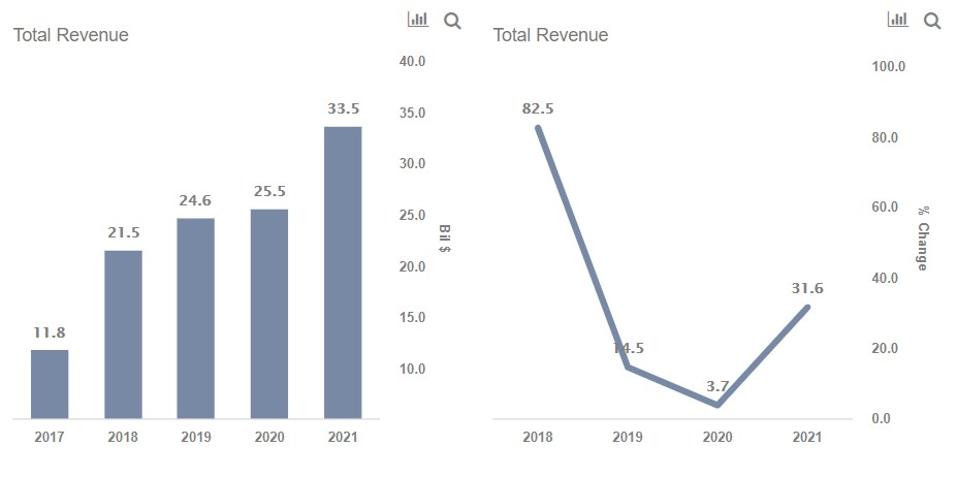

For more details on the outlook for Tesla’s revenues, view our dashboard analysis Tesla Revenues: How Does TSLA Make Money?

What Are Regulatory Credits And How Do They Help Tesla?

Several U.S. states and countries have Zero Emissions Vehicle regulations that require that clean vehicles account for a certain mix of auto manufacturers’ sales each year. If automotive companies, which still largely sell internal combustion engine-based vehicles, don’t meet these standards, they can buy credits from the likes of Tesla that earn credits, as they only sell electric vehicles. Although the revenues from these credits are quite volatile they are very lucrative for Tesla, as it likely incurs no direct costs to earn them. The bump in these regulatory credit sales is likely to be partly responsible for the company’s automotive gross margins expanding 300 bps sequentially to 25.5%. While it’s possible that such credits could become more valuable in the medium term, as new emissions regulations come into play in Europe and states in the U.S. look to enforce stricter norms, the current collapse in global auto sales could hurt revenues from ZEV credits in the near-term for Tesla.

Outlook Remains Tough For Tesla In The Near-term

Tesla is likely to face significant near-term revenue pressure and the company has put its 2020 guidance on hold, due to uncertainty surrounding the coronavirus pandemic and the broader economic recovery. There is little reason for people to buy expensive cars right now and Tesla’s production at its Fremont facility, which accounts for about three-quarters of its annual capacity, remains suspended and there’s no clarity as to when it could resume.

However, despite significant near-term headwinds, the company’s stock has continued to rally, almost doubling year-to-date. The company trades at a P/S multiple of about 6x, compared to GM which trades at about 0.3x, based on trailing revenues. This means that the stock has significant valuation risk, making it react more strongly to negative news compared to its peers.

Our theme Autos Fight COVID-19 contrasts the performance of Tesla stock, which is up almost 90% YTD, with mainstream automakers, who have seen their stocks fall by about 40%.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Read Again https://www.forbes.com/sites/greatspeculations/2020/05/04/tesla-banked-on-emission-credits-for-q1-beat-but-outlook-is-tough/Bagikan Berita Ini

0 Response to "Tesla Banked On Emission Credits For Q1 Beat, But Outlook Is Tough - Forbes"

Post a Comment